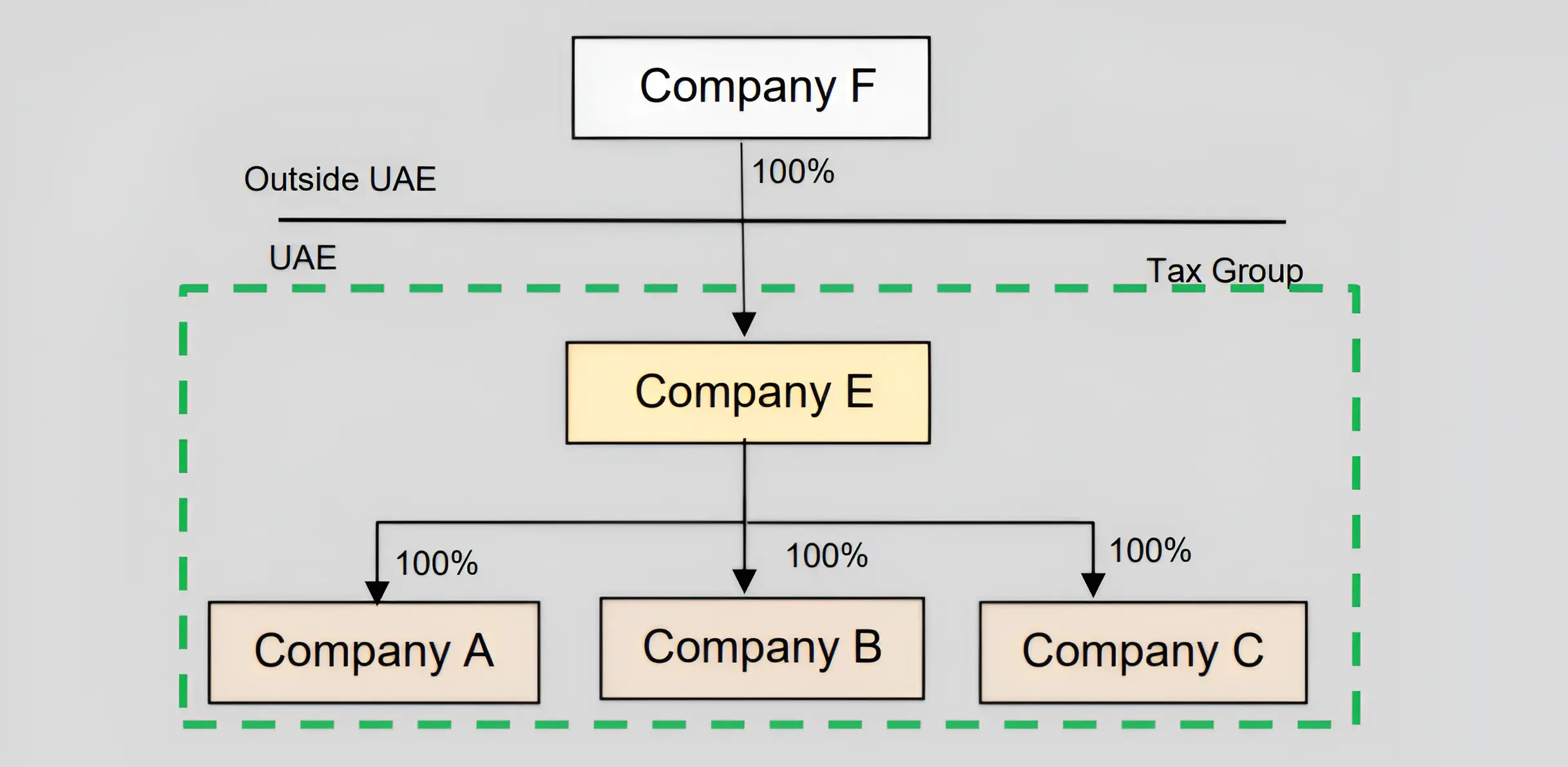

Example 1: Resident Subsidiaries of a foreign parent forming a Tax Group

Website Last updated:

July 3, 2026

1. Glossary

2. Introduction

2.1. Overview

2.2. Purpose of this guide

2.3. Who should read this guide?

2.4. How to use this guide

2.5. Legislative references

2.6. Status of this guide

3. What is a Tax Group?

4. Conditions to form a Tax Group

4.1. Juridical persons condition

4.2. Resident Persons condition

4.2.1. Resident Person under the Corporate Tax Law and under Double Taxation Agreements

4.2.2. Dual resident persons

4.2.3. Documentation to prove tax residence

4.2.4. Parent Company held by a non-resident person

4.3. Share capital ownership condition

4.3.1. What is share capital?

4.3.2. Ownership of share capital

4.3.3. Determining the 95% share capital ownership threshold

4.3.4. Indirect ownership

4.3.5. Transfer of shares between members of a Tax Group

4.3.6. Transfer of shares outside the Tax Group

4.4. Voting rights condition

4.4.1. General

4.4.2. Extraordinary voting rights

4.4.3. Indirect holding of voting rights

4.5. Profits and net assets condition

4.5.1. Profits condition

4.5.2. Entitlement to at least 95% of the Subsidiary’s net assets

4.5.3. Impact of different share classes

4.5.4. Transfer of shares outside the Tax Group

4.5.5. Indirect holding of rights to profits or net assets

4.6. Exempt Person condition and Qualifying Free Zone Person condition

4.6.1. General

4.6.2. Exception for Government Entities

4.6.3. Small Business Relief

4.7. Financial Year condition

4.7.1. General

4.7.2. Newly established juridical person joining a Tax Group

4.7.3. Change of Tax Period in order to form or join a Tax Group

4.8. Accounting Standards condition

5. Forming a Tax Group and tax compliance obligations

5.1. Application to FTA to form a Tax Group

5.2. Responsibilities of the Parent Company of a Tax Group

5.3. Liability for Corporate Tax Payable

5.4. Tax Registration of the Tax Group and members of the Tax Group

5.5. Tax Deregistration of the Tax Group and members of the Tax Group

6. Change in members of a Tax Group

6.1. General

6.2. Joining a Tax Group

6.2.1. Subsidiary joins a Tax Group

6.2.2. Newly incorporated entity joins a Tax Group

6.3. Leaving a Tax Group

6.3.1. General

6.3.2. Subsidiary ceases to exist upon transfer of Business

6.4. Change of the Parent Company of a Tax Group

6.5. Compliance impact of changes in a Tax Group

6.5.1. Tax Deregistration

6.5.2. Financial Statements

7. Cessation of a Tax Group

7.1. General

7.2. Tax Deregistration of a Tax Group