Website Last updated:

July 3, 2026

Business Restructuring Relief

Corporate Tax Guide | CTGBRR1

April 2024

Contents

1. Glossary

2. Introduction

2.1. Overview

2.2. Purpose of this guide

2.3. Who should read this guide?

2.4. How to use this guide

2.5. Legislative references

2.6. Status of this guide

3. Business Restructuring Relief: General Aspects

3.1. Overview of transactions covered in scope of Business Restructuring Relief

3.2. Examples of Business restructuring transactions covered under Article 27(1)(a) of the Corporate Tax Law

3.3. Examples of transactions covered under Article 27(1)(b) of the Corporate Tax Law

3.4. Examples of transactions not covered under Business Restructuring Relief

3.5. Meaning of Business or independent part of a Business

3.6. Consideration for transfer

3.6.1. Recipient of consideration

3.6.2. Payer or issuer of consideration

3.6.3. Form of consideration

3.6.4. Situations where no consideration is required

4. Conditions to qualify for Business Restructuring Relief

4.1. Legally compliant condition

4.2. Taxable Persons condition

4.3. Exempt Person condition and Qualifying Free Zone Person condition

4.4. Financial Year condition

4.5. Accounting Standards condition

4.6. Valid commercial reasons condition

5. Consequences of electing for Business Restructuring Relief

5.1. Transfer of assets and liabilities at net book value

5.1.1. Determining net book value of assets and liabilities transferred

5.1.2. Adjustments to be made by the Transferee

5.2. Value of shares or ownership interest received

5.3. Transfer of Tax Losses

5.4. Consequences of not meeting requirements or not electing for Business Restructuring Relief

6. Clawback of Business Restructuring Relief

6.1. Transfer of shares in the Transferor or Transferee

6.1.1. Situations where transfer of shares will trigger clawback of relief

6.1.2. Clawback in the context of the transfer of shares

6.2. Subsequent transfer of Business

6.2.1. Situations where Business Restructuring Relief is not clawed back

6.3. Consequences of the clawback

6.3.1. Consequences in hands of the Transferor

6.3.2. Consequences in hands of the Transferee

7. Compliance requirements

7.1. Election by Transferor

7.2. Record keeping

8. Interaction of Business Restructuring Relief with other parts of Corporate Tax Law

8.1. Qualifying Group Relief

8.2. Realisation basis

8.3. Transitional relief

9. Updates and Amendments

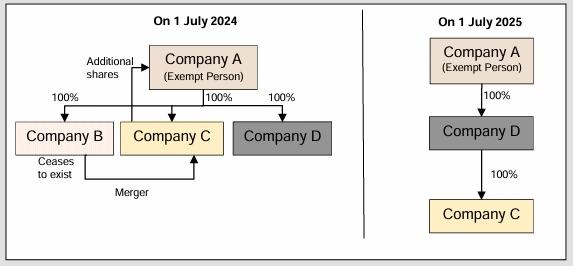

Company A, Company B, Company C and Company D are companies incorporated and resident in the UAE and who all use the Gregorian calendar year as their Financial Year and Tax Period. Company A is an Exempt Person as a Government Controlled Entity. Before 1 July 2024, Company A held 100% of the shares in Company B, Company C and Company D.

Company A, Company B, Company C and Company D are companies incorporated and resident in the UAE and who all use the Gregorian calendar year as their Financial Year and Tax Period. Company A is an Exempt Person as a Government Controlled Entity. Before 1 July 2024, Company A held 100% of the shares in Company B, Company C and Company D.