Input Tax Apportionment

VATGIT1

September 2025

Contents

3. Overview of Input Tax apportionment

4. Special apportionment methods

5. Specified Recovery Percentage

6. Applying for special apportionment method and/or SRP

Glossary

AED | : | The United Arab Emirates Dirham. |

Applicant | : | A Person applying to use a special Input Tax apportionment method or specified recovery percentage. |

Apportionment Rate | : | The percentage of Residual Input Tax qualifying for Input Tax recovery. |

Business | : | Any activity conducted regularly, on an ongoing basis and independently by any Person, in any location, such as industrial, commercial, agricultural, professional, vocational, service or excavation activities or anything related to the use of tangible or intangible properties. |

Business Day | : | Any day of the week, except weekends and official holidays of the Federal Government. |

Decree-Law | : | Federal Decree-Law No. 8 of 2017 on Value Added Tax and its amendments. |

Executive Regulation | : | Cabinet Decision No. 52 of 2017 on the Executive Regulation of the Federal Decree-Law No. 8 of 2017 on Value Added Tax, and its amendments. |

Exempt Supply | : | A supply of Goods or Services for Consideration while conducting Business in the UAE, where no Tax is imposed and the Input Tax related thereto is not recovered, except according to the provisions of the Decree-Law. |

FTA | : | Federal Tax Authority, being the Authority responsible for the administration, collection and enforcement of federal taxes in the UAE. |

FTA Decision No. 2 | : | Federal Tax Authority Decision No. 2 of 2025 on the Authority's Policy on Issuing Clarifications and Directives. |

Input Tax | : | Tax paid by a Person or due from him when Goods or Services are supplied to him, or when conducting an Import. |

Legal Representative | : | The guardian or custodian of an incapacitated person or minor, or the bankruptcy trustee appointed by the court for a company that is in bankruptcy, or any other Person legally appointed to represent another Person. |

Person | : | A natural or legal person. |

Payable Tax | : | Tax that is due for payment to the FTA. |

Recoverable Input Tax | : | Amounts that have been paid and that the FTA may return to the Taxpayer pursuant to the provisions of the Decree-Law. |

Registrant | : | The Taxable Person who has been issued with a TRN. |

Residual Input Tax | : | Input Tax that is partly attributable to the making of supplies that give the right for full Input Tax recovery, i.e. Taxable Supplies, and partly attributable to supplies for which Input Tax is non-recoverable, i.e. Exempt Supplies and/or non-business activities. |

Specified Recovery Percentage (SRP) | : | An Input Tax recovery rate that is calculated based on the Registrant's recovery rate in the previous Tax year. |

Tax | : | Value Added Tax (VAT). |

Tax Agent | : | Any Person registered with the FTA who is appointed on behalf of another Person to represent him before the FTA and assist him in the fulfilment of his obligations and the exercise of his associated Tax rights. |

Tax Group | : | Two or more Persons registered with the FTA for Tax purposes as a single Taxable Person in accordance with the provisions of the Decree-Law. |

Tax Period | : | A specific period of time for which the Payable Tax shall be calculated and paid. |

Taxable Supply | : | A supply of Goods or Services for Consideration during the course of Business by any Person in the UAE, and does not include Exempt Supply. |

Tax Registration Number (TRN) | : | A unique number issued by the FTA for each Person registered for Tax purposes. |

UAE | : | United Arab Emirates. |

Wholly Recoverable Input Tax | : | Value of Input Tax which is directly and wholly attributable to supplies for which VAT may be recovered in accordance with the Article 54(1) of the Decree-Law. |

Introduction

Short brief

VAT is a general consumption tax on the supply of Goods and Services, that applies to most supplies which take place within the territorial area of the UAE.

Purpose of this document

The purpose of this Guide is to provide guidance on Input Tax apportionment and the special Input Tax apportionment methods which may be used by certain types of entities where the standard Input Tax-based apportionment method does not yield a fair and reasonable result.

The Guide provides:

an overview of the general Input Tax apportionment rules, the available special methods of Input Tax apportionment, and the determination of the SRP, and

an overview of the process to apply for approval to use a special Input Tax apportionment method and/or the SRP.

For any additional questions regarding the process to apply for approval to use a special Input Tax apportionment method and/or the SRP, please contact info@tax.gov.ae.

Who should read this document?

This document should be read by any Registrant who makes a mixture of Taxable Supplies and Exempt Supplies or non-business activities, and any other Person responsible for or involved with the apportionment calculation for such a Business.

Legislative references

In this Guide, the following legislation will be referred to as follows:

Federal Decree-Law No. 8 of 2017 on Value Added Tax and its amendments is referred to as "Decree-Law",

Federal Decree-Law No. 28 of 2022 on Tax Procedures and its amendments is referred to as "Tax Procedures Law",

Cabinet Decision No. 52 of 2017 on the Executive Regulation of the Federal Decree-Law No. 8 of 2017 on Value Added Tax, and its amendments, is referred to as "Executive Regulation",

Cabinet Decision No. 74 of 2023 on the Executive Regulation of Federal Decree-Law No. 28 of 2022 on Tax Procedures is referred to as "Tax Procedures Executive Regulation",

Federal Tax Authority Decision No. 8 of 2022 on the Special Methods of Input Tax Apportionment is referred to as "FTA Decision No. 8", and

Federal Tax Authority Decision No. 2 of 2025 on the Authority's Policy on Issuing Clarifications and Directives is referred to as "FTA Decision No. 2".

Status of the Guide

This Guide is not a legally binding document, but is intended to provide assistance in understanding and applying the VAT legislation with regards to Input Tax apportionment, special methods for Input Tax apportionment, and the SRP.

The information provided in this Guide should not be interpreted as legal or Tax advice. It is not meant to be comprehensive and does not provide a definitive answer in every case. It is based on the legislation as it stood when the Guide was published. Each Person's own specific circumstances should be considered.

The Decree-Law, Executive Regulation, and FTA Decisions referred to in this document will set out the principles and rules that govern the application of Input Tax apportionment, special methods for Input Tax apportionment, and SRP. Nothing in this publication modifies or is intended to modify the requirements of any legislation.

This document is subject to change without notice.

Overview of Input Tax apportionment

Introduction

Persons conducting Business activities in the UAE incur VAT on Goods and Services, which is referred to as Input Tax. Registrants can recover Input Tax via the normal Tax Return process, subject to certain conditions being met. Consequently, VAT should, generally, not be a cost to a Registrant where such expenditure is incurred to make Taxable Supplies. However, where the Taxable Person is not able to recover the VAT incurred in respect of Goods or Services, the Person is, in effect, treated as the end consumer of those Goods or Services, and VAT becomes a cost to the Business.

Entitlement to recover Input Tax

A Registrant is entitled to recover Input Tax incurred on the purchase of Goods and Services to the extent such Goods and Services are used, or intended to be used, in making any of the following:[1]

Taxable Supplies,

supplies that are made outside the UAE which would have been considered taxable had they been made in the UAE, and

supplies of financial Services which would have been treated as exempt if made in the UAE, but which are provided to a Person who is outside the UAE at the time of the supply, and the Services are treated as taking place outside the UAE.[2]

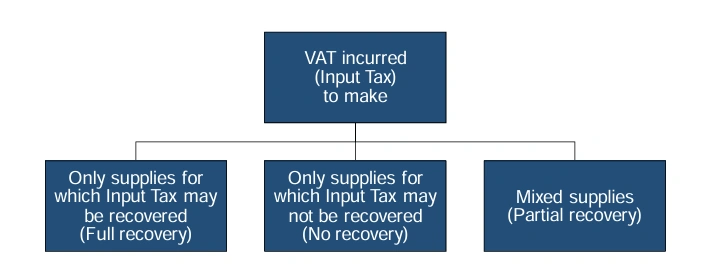

A Taxable Person is entitled to full Input Tax recovery in respect of Goods and Services wholly used (or intended to be used solely) for any of the above purposes. In contrast, where the Goods or Services are used (or intended to be used) solely for non-business purposes or to make wholly Exempt Supplies, the Person will not be able to recover any of the Input Tax incurred.

In certain circumstances, Goods or Services will be used partly in the course of making supplies that allow the recovery of Input Tax and partly for other purposes that do not allow Input Tax recovery. Where an expense is incurred for the making of such mixed supplies, the Taxable Person must determine the actual portion of the Input Tax on the expense that can be recovered.

Input Tax apportionment per Tax Period

Input Tax which is incurred in respect of Goods or Services which are used partly for making supplies that allow for VAT recovery and partly for other purposes for which VAT is not recoverable is referred to as "Residual Input Tax". Residual Input Tax must be apportioned between those activities. Recovery will be restricted to the portion relating to supplies that allow for VAT recovery.

Step 1: Direct attribution

To identify the amount of the Residual Input Tax, the Input Tax which is either recoverable or non-recoverable in full has to be excluded. Therefore, the first step is to perform the following calculations in respect of each Tax Period:[3]

Calculate the total value of Input Tax which is directly attributable to supplies for which VAT may be recovered under Article 54(1) of the Decree-Law, i.e. Wholly Recoverable Input Tax.

Calculate the total value of Input Tax which is directly attributable to supplies for which VAT cannot be recovered.

Note that Input Tax which is specifically blocked under Article 53 of the Executive Regulation shall be excluded from this calculation.

Step 2: Residual Input Tax

Any Input Tax incurred which cannot be directly attributed to the making of supplies in respect of which Input Tax is wholly recoverable or wholly non-recoverable constitutes the Residual Input Tax of the Taxable Person.

Step 3: Apportionment Rate

The next step is to determine the percentage of Residual Input Tax that may be recovered, i.e. the Apportionment Rate. The standard method for apportioning the Residual Input Tax, as described in Article 55(6) of the Executive Regulation, is referred to as the inputs-based apportionment method and is calculated as follows:

a(a + b)× 1001

Where:

a = Wholly Recoverable Input Tax

b = Wholly non-recoverable Input Tax

The percentage should be rounded to the nearest whole number.[4]

Examples of rounding:

Recovery percentage | Rounded to the nearest whole number |

90.87% | 91% |

61.50% | 62% |

73.19% | 73% |

Step 4: Recoverable Input Tax

The recoverable portion of the Residual Input Tax is calculated by multiplying the total value of Residual Input Tax by the Apportionment Rate calculated under Step 3 above.

To calculate the total Recoverable Input Tax for the Tax Period, the recoverable portion of the Residual Input Tax shall be added to the Wholly Recoverable Input Tax determined under Step 1.

This calculation is required to be performed for each Tax Period in which the Taxable Person incurs Input Tax relating to the making of Exempt Supplies, or to activities that are not in the course of Business,[5] unless the Registrant obtained approval from the FTA to use the SRP.

Input Tax apportionment – Annual adjustments

Registrants are required to perform two additional calculations at the end of each Tax year. The Registrant's Tax year is determined by the registration stagger and may be different than the calendar year and the Registrant's financial year.[6]

Staggers | Tax Periods | Tax year-end |

VAT Stagger 1 | Feb – Apr, May – Jul, Aug – Oct, Nov – Jan | 31 January of every year |

VAT Stagger 2 | Mar – May, Jun – Aug, Sep – Nov, Dec – Feb | Last day of February every year |

VAT Stagger 3 | April – Jun, Jul – Sep, Oct – Dec, Jan – Mar | 31 March of every year |

VAT Stagger 4 | Monthly | 31 December of every year |

If the Registrant's Tax year ends on a date other that the financial year-end, the Registrant may submit a request to the FTA via EmaraTax to amend the stagger to align these two dates.

The first calculation is to perform an annual washup and the second is to calculate an actual use adjustment. If the FTA approved the use of a special apportionment method, the Registrant is not required to calculate the actual use adjustment for the Tax years during the validity period of the approved decision.

Special cases for Tax year-end

As Registrants are assigned Tax Periods in staggers as outlined above, each Registrant is required to determine its Tax year-end accordingly. In certain cases, a Registrant's Tax year-end may differ from the registration stagger assigned. Article 55(4) of the Executive Regulation specifies the following special cases which trigger the end of a Tax year:

# | Special case | Tax year-end |

1 | Deregistration | The last day on which the Registrant is a Taxable Person. |

2 | Joining a Tax Group | The last day before the Registrant joins the Tax Group, i.e. the day before the effective date of joining the Tax Group. |

3 | Leaving a Tax Group | The last day before the member left the Tax Group, i.e. the day before the effective date of the Tax Group's amendment. |

Annual washup and actual use adjustment

At the end of the Registrant's Tax year, the Registrant is required to perform an annual washup calculation as described below and report the result in the adjustment column of Box 9 of the first Tax Return following the end of the Registrant's Tax year:

Step 1: Combine Input Tax recovered in returns submitted during Tax year

Combine the Input Tax recovered during each of the Tax Periods forming part of that Tax year by adding Boxes 9 and 10 of all the relevant Tax Returns submitted together.

Step 2: Recalculate Recoverable Input Tax

Recalculate Recoverable Input Tax for the Tax year as if it was a single Tax Period.[7] The same principles (i.e. direct attribution and Residual Input Tax) apply as in Step 1 of Section 3.3. Note that the amount of the Residual Input Tax should remain the same, but the Apportionment Rate for this calculation may vary as the intention is to smoothen the percentage by removing, for example, seasonal fluctuations. In instances where the FTA approved the use of a special apportionment method, the annual washup calculation shall be performed using the approved special apportionment method, until the expiry of the approved decision.

Step 3: Calculate annual washup adjustment

Deduct the total Recoverable Input Tax calculated in Step 1 from the amount calculated in Step 2 to calculate the annual washup adjustment.

Kindly note that, for the purpose of calculating the annual washup adjustment, there is no threshold on the adjustment amount arising from the annual washup calculation. Consequently, the resulting adjustment may be either positive or negative.

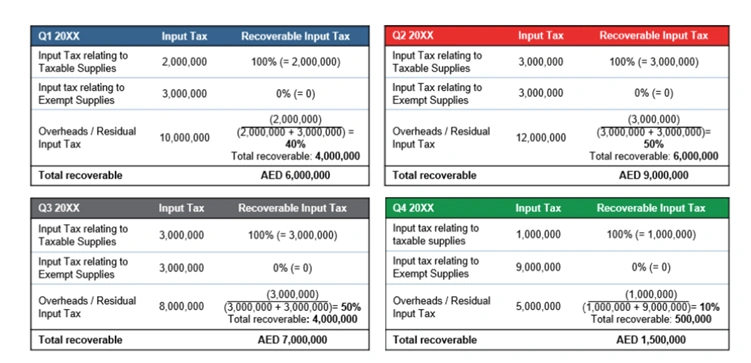

Example 1

Company A, a small retail bank, is a Registrant that makes both Taxable Supplies and Exempt Supplies. Company A incurs Input Tax related to wholly Taxable Supplies, Input Tax related to wholly Exempt Supplies, and Input Tax used for mixed purposes (i.e. Residual Input Tax).

Tax year | Wholly Recoverable Input Tax | Wholly non-recoverable Input Tax | Residual Input Tax |

Quarter 1 | 2,000,000 | 3,000,000 | 10,000,000 |

Quarter 2 | 3,000,000 | 3,000,000 | 12,000,000 |

Quarter 3 | 3,000,000 | 3,000,000 | 8,000,000 |

Quarter 4 | 1,000,000 | 9,000,000 | 5,000,000 |

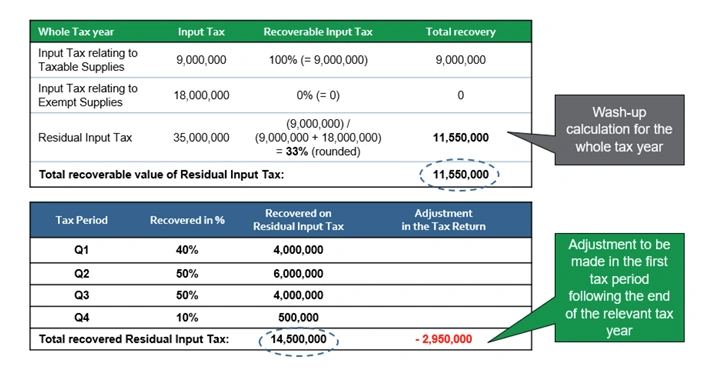

Total | 9,000,000 | 18,000,000 | 35,000,000 |

The Recoverable Input Tax per the Tax Returns is as follows:

The total Residual Input Tax recovered per the Tax Returns submitted for the calendar year is AED 14,500,000.[8]

Based on the above, the annual washup adjustment is calculated as the difference between the recoverable Residual Input Tax per the returns submitted (AED 14,500,000) and the recoverable Residual Input Tax per the annual calculation (AED 11,550,000), i.e. AED 2,950,000. In this case an excess amount of Input Tax was recovered via the Tax Returns.

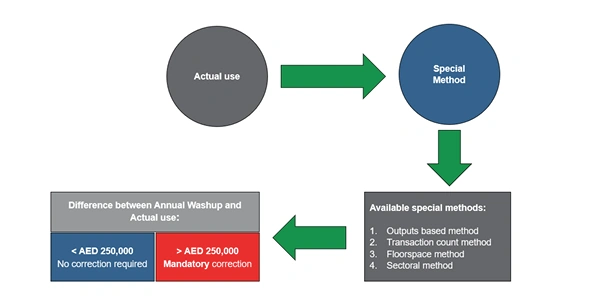

Actual use adjustment

After performing the annual washup calculation, the Registrant is required to calculate the difference between the Recoverable Input Tax per the annual washup calculation and the Input Tax which would have been recoverable if an Apportionment Rate based on actual use was used.

The Registrant shall only make an actual use adjustment where the difference in the Recoverable Input Tax amounts between the annual washup and the actual use calculations exceeds AED 250,000.[9]

Example 2

Registrant | Recoverable Residual Input Tax | Variance | Actual use adjustment required | |

Annual washup calculation | Actual use calculation | |||

Company 1 | 900,000 | 500,000 | 400,000 | Yes |

Company 2 | 900,000 | 750,000 | 150,000 | No |

Company 3 | 900,000 | 1,200,000 | (300,000) | Yes |

Company 4 | 900,000 | 1,000,000 | (100,000) | No |

If the Registrant's Tax year is less than 12 months, the AED 250,000 needs to be prorated accordingly.[10] For example, if the Business is newly established and its Tax year consisted of only nine months, the AED 250,000 threshold is reduced to AED 187,500 (e.g. AED 250,000 × 9/12).

Kindly note, that for purposes of the actual use calculation, the Registrant is required to use one of the special apportionment methods described in Chapter 4 in this Guide, taking into account the guidelines on which special methods can be used by certain types of Businesses.

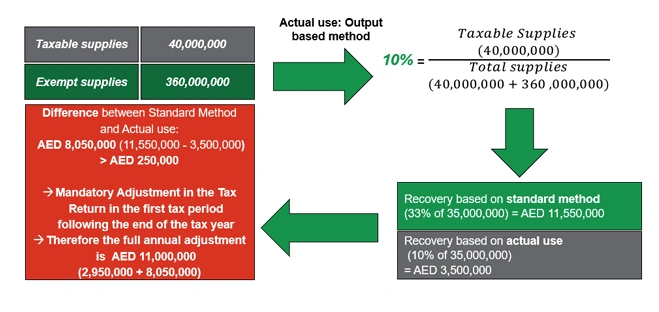

Example 3

Company A (same as in Example 1) is eligible to use the outputs-based special method for determining whether an actual use adjustment is required. Company A made the following supplies during its Tax year:

Taxable Supplies: AED 40,000,000

Exempt Supplies: AED 360,000,000

Residual Input Tax per annual washup calculation: AED 35,000,000

Recoverable Residual Input Tax per annual washup calculation: AED 11,550,000

Step 1: Calculate the recoverable Residual Input Tax based on the alternative special method

The Residual Input Tax recovery rate, using the outputs-based method[11] is calculated as follows:

Taxable Supplies (40,000,000)Taxable Supplies (40,000,000) + Exempt Supplies (360,000,000)× 1001= 10%

The recoverable Residual Input Tax under this method is AED 35,000,000 × 10% = AED 3,500,000.

Step 2: Calculate the difference between recoverable Residual Input Tax per the annual washup and actual use calculations

Recoverable Residual Input Tax per annual washup calculation | AED 11,550,000 |

Less: recoverable Residual Input Tax per actual use calculation | (AED 3,500,000) |

Difference | AED 8,050,000 |

Step 3: Determine whether an actual use adjustment is required

Since the variance calculated in Step 2 is more than AED 250,000, Company A is required to make an actual use adjustment.

Step 4: Calculate the total year-end adjustment related to recoverable Residual Input Tax

Company A is required to reduce its Input Tax recovery in the adjustments' column in its first Tax Return of the following Tax year, by the following:

Annual washup adjustment: | AED 2,950,000 |

Actual use adjustment: | AED 8,050,000 |

Total | AED 11,000,000 |

In summary:

Special apportionment methods

Introduction

The FTA accepts that the standard inputs-based apportionment method may not be appropriate for every Registrant and its sector(s) of operation. Each Business is different, and the standard method of apportionment may give rise to outcomes that do not accurately reflect the actual use of Goods and/or Services acquired by the Registrant.

In such cases, Registrants may apply for an alternative method of Input Tax apportionment to be used.[12] If a special Input Tax apportionment method is approved by the FTA, the Registrant shall apply the approved method from the first Tax Period following the Tax Period in which the approval was granted by the FTA.[13] In the case of a Tax Group, the special apportionment method shall apply to the whole Tax Group as all the members of a Tax Group are regarded being a single Person represented by the representative member of the Tax Group.[14]

The special Input Tax apportionment methods which are available to Registrants are:

Outputs-based method,

Transaction count method,

Floorspace method, and

Sectoral method.

Not every special Input Tax apportionment method will be available to every Business as FTA Decision No. 8 specifies which types of Businesses are eligible for each of the approved special Input Tax apportionment methods. This Chapter provides a summary of the Businesses that are eligible for each of the approved special Input Tax apportionment methods in accordance with FTA Decision No. 8.

Furthermore, should the FTA consider that the standard inputs-based apportionment method does not reflect the actual extent to which the Registrant's Input Tax incurred relates to making Taxable Supplies, the FTA may require the Registrant to submit an application for the use of the appropriate special apportionment method.[15] For example, if the FTA finds during an audit that a financial institution is using the standard Input Tax-based apportionment method although the Taxable Person operates across multiple sectors, which may include real estate, retail banking and investment banking, the FTA may require that the Registrant apply to use the sectoral apportionment method.

Where a special method is approved, it will be applied for each Tax Period following the date of approval as well as for the annual washup adjustment in the first Tax Period of the following Tax year. Furthermore, on the basis that the special apportionment method already considers the actual use of Goods and Services, no actual use adjustment will be required in respect of Tax years following the approval as long as the FTA approval remains valid. The approval will typically be granted for four years in the case of a non-sectoral method and for two years in the case of the sectoral method.

Eligible Persons

Registrants that have been registered for VAT for at least six months[16] may apply for approval to use a special apportionment method to determine the recoverable portion of Residual Input Tax.

An application to use a special Input Tax apportionment method may only be submitted by any of the following Persons:

the authorised signatory of the Registrant, or the Registrant itself if the Registrant is a natural Person,

the authorised signatory of the representative member of a Tax Group,

a Tax Agent appointed by the Registrant, or

the Legal Representative appointed by the court.

Kindly note that applications submitted by any other Person (such as a tax consultant, or natural Person submitting a request on behalf of a Registrant) will not be accepted.

Conditions for eligibility

All of the following conditions must be met for the FTA to objectively review the application to use a special method for Input Tax apportionment:[17]

The Applicant has been a Registrant for at least 6 months.

The Applicant is making supplies for which they may recover the Input Tax and other supplies for which they may not recover the Input Tax.

The Applicant can demonstrate that the standard inputs-based apportionment method does not yield a fair and reasonable result with regard to the recovery of Input Tax, and submits the required supporting documentation as part of the application.

The Registrant is requesting to use a special apportionment method that is available to the type of Business in accordance with FTA Decision No. 8. The special apportionment methods, including the eligible Businesses are addressed below.

Outputs-based method

How does it work?

The outputs-based method determines the Apportionment Rate for Residual Input Tax on the basis of the types of supplies made by the Taxable Person.

To calculate the recovery ratio under this method, the Registrant needs to identify the value of Taxable Supplies as a proportion of all supplies made by the Taxable Person (including non-business activities).

Value of taxable suppliesTotal value of supplies× 1001

This method is appropriate where the VAT incurred by a Business is mostly directly linked to income earned, i.e. where there is a strong correlation between income and expenses.

Eligible Businesses

The outputs-based method is available for Businesses engaged in the following sectors:

Educational institutions,

Establishments that conduct non-business activities, such as art galleries, cultural entities,

Financial institutions, such as banks that provide banking Services to individuals, companies, large establishments and investment banks, and similar institutions (Islamic and non-Islamic),

Insurance companies (Islamic and non-Islamic), or

Local passenger transportation Service providers.

Transaction count method

How does it work?

The transaction count method determines the Apportionment Rate based on the number of taxable transactions as a proportion of all transactions carried out by the Business during the period.

Number of taxable transactionsTotal number of transactions× 1001

The transaction count method is used when the VAT on expenses incurred by the Business is most directly linked to the number of transactions (i.e. supplies made) rather than the amount of income earned – that is, where the level of expense would be similar regardless of the value of the supplies being made.

This method will only be appropriate if the nature of the transactions is such that each transaction is either wholly taxable or wholly exempt. Any transactions with both taxable and exempt components should be excluded from the transaction count calculation.

In order to use this method, the Registrant is required to accurately define the type of transactions as well as the related Tax treatment in order to provide a clear audit trail to support the apportionment calculation.

Furthermore, the Registrant is not permitted to selectively choose transactions but must clearly define all the transactions of the Business that generate income, directly and indirectly. Once the transactions are identified, the Registrant must also clearly explain how the transactions are counted at the time of application.

The Registrant is, therefore, required to ensure that their accounting or management system is able to identify and track the different types of transactions.

Eligible Businesses

The transaction count method is available to financial institutions, such as banks (Islamic and non-Islamic), that provide banking Services to companies, large establishments and investment banks, and similar institutions.

Floorspace method

How does it work?

The floorspace method determines the Apportionment Rate for Residual Input Tax by identifying the proportion of the floorspace used for taxable activities as a percentage of the total floorspace used by the Business, excluding areas used for both taxable and non-taxable purposes, e.g. communal spaces, elevator shafts and lobbies.

Floorspace for making Taxable SuppliesTotal floorspace× 1001

The measuring unit used for the nominator and denominator should be consistent, e.g. if using square metres (m2) for the numerator, m2 should also be used for the denominator.

The floorspace method is used when it is possible to identify whether a specific area is used for a taxable or non-taxable/exempt activity.

Eligible Businesses

The floorspace method is available to landlords and Businesses dealing with supplies (sales and rental) of commercial and residential properties, including real estate companies and other Businesses selling or renting out real estate on an ongoing basis, where expenses would be similar for floorspace regardless of whether used for making Taxable Supplies, Exempt Supplies, or non-taxable supplies.

Sectoral method

How does it work?

Large complex Businesses and Tax Groups may conduct different Business activities through different divisions which are independent of each other from an operational and accounting perspective. For example, a bank may have different divisions dealing with retail customers and investment banking, or an insurance company may, in addition to its core Business, have a real estate division which deals with renting out of properties. In the case of Tax Groups, the members may conduct diverse Businesses in various sectors, including financial Services, real estate, retail etc.

Where such Business activities are conducted through distinct divisions of a single entity or Tax Group, and different expenses relate to activities of these divisions, none of the above special apportionment methods may be suitable for apportioning Input Tax for the Business or Tax Group as a whole. To ensure that the apportionment method is appropriately tailored to each of the distinct Business divisions, such Businesses may apply for a "sectoral" method of Input Tax apportionment.

The sectoral method involves the following steps:

The Taxable Person must identify the Residual Input Tax in accordance with the provisions of Article 55 of the Executive Regulation as described in this Guide.

Any Residual Input Tax which relates wholly to a particular sector (i.e. division or entity) should be allocated wholly to that sector.

The remaining Residual Input Tax which relates to more than one sector should be divided between those sectors in accordance with an appropriate allocation method (discussed below).

Each of the sectors should then be assigned an appropriate special Input Tax apportionment method for that specific sector (e.g. the standard input-based apportionment method, outputs-based method, transaction count method or the floorspace method). This assigned method would then be used by the sector to apportion the Residual Input Tax relating to that sector.

Sector allocation methods

Where the Residual Input Tax of a Business relates to multiple sectors of that Business, it is necessary to allocate the Input Tax to these individual sectors. There are two methods which can be used for such an allocation:

Headcount method, and

Outputs method.

Headcount method

The headcount method is used when overhead expenses incurred are most closely related to the number of employees, i.e. if the expenses are linked to employees. For example, an insurance company may have different employees solely working in its life and general insurance divisions.

The headcount method uses the full-time equivalent (FTE) of staff (usually income generating only, not back office) employed or used in each sector. In instances where employees work in more than one department/division/unit, the staff numbers shall be measured on an FTE basis.

Number of FTE members in the relevant sectorTotal number of FTE

Outputs method

The outputs method is best used when expenses are linked to income. The amount of income in the sector may, therefore, be reflective of the Input Tax incurred on expenses. The allocation under this method is done using the following formula:

Value of sector's suppliesTotal value of supplies× 1001

This method can be appropriate for a wide-range of entities in both private and not-for-profit sectors. However, it may not be appropriate where the Business has a mixture of well-established sectors and sectors in a start-up phase, as the expectation would be that the start-up divisions would have proportionally more expenses than income.

Eligible Businesses

It is expected that sectoral methods will be used by large, complex companies and establishments with different divisions, such as:

Financial Institutions such as banks with retail, investment and real estate divisions, and similar institutions,

Insurance companies providing both life and non-life insurance,

Real estate companies that have separate divisions for commercial and residential properties.

Summary of available special apportionment methods

Please refer to the following table which reflects the apportionment methods that are available to different types of Businesses per FTA Decision No. 8. The FTA will reject applications where the Applicant has applied for a special Input Tax apportionment method which is not applicable to its specific type of Business.

# | Special method | Eligible Business sectors |

1 | Outputs-based | • Educational institutions. |

2 | Transaction count | • Financial institutions, such as banks (Islamic and non-Islamic), that provide banking Services to companies, large establishments and investment banks, and similar institutions. |

3 | Floorspace | • Landlords and Businesses dealing with supplies (sales and rental) of commercial and residential properties. |

4 | Sectoral | • Financial institutions, such as banks with retail, investment and real estate divisions, and similar institutions. |

Specified Recovery Percentage

Introduction

The Executive Regulation was amended and, from 15 November 2024, Taxable Persons may apply to use an SRP to apportion the Residual Input Tax.[18]

Subject to FTA's approval, an SRP is determined based on the recovery rate at the end of each preceding Tax year and applied to the subsequent Tax year's Tax Periods, rather than having to calculate the relevant Apportionment Rate for each Tax Period.

Eligible Persons

Registrants that have been registered for VAT for at least 12 months[19] may apply for approval to use an SRP.

The request may only be submitted by any of the following Persons:

the authorised signatory of the Registrant, or the Registrant itself if the Registrant is a natural Person,

the authorised signatory of the representative member of a Tax Group,

a Tax Agent appointed by the Registrant, or

the Legal Representative appointed by the court.

Kindly note that applications submitted by any other Person (such as a tax consultant, or natural Person submitting a request on behalf of a Registrant) will not be accepted.

Conditions for eligibility

To be eligible to apply for the use of an SRP, all of the following conditions must be met:

the Applicant has been registered for VAT for at least 12 months, and

the Applicant is making supplies for which they may recover the Input Tax and other supplies for which they may not recover the Input Tax.

How does it work?

Approval of an SRP allows the Registrant to calculate the SRP based on the preceding Tax year and apply it to the Tax Periods of the subsequent Tax year, rather than having to calculate an Apportionment Rate for each Tax Period.

The SRP is determined on the following basis:

If the nature of the Registrant's Business is such that a special apportionment method prescribed by the FTA may be applicable to that Business, and there is approval from the FTA to use such method, the SRP should be the preceding Tax year's calculated recovery rate based on the relevant special apportionment method.

If the nature of the Registrant's Business is such that a special apportionment method prescribed by the FTA may be applicable to that Business, but the Registrant has not applied to use such special apportionment method, the application should be for the SRP based on the relevant special apportionment method.

If the nature of the Registrant's Business is such that none of the special apportionment methods can be applicable to the Business, the SRP is based on the preceding Tax year's calculated recovery rate, which is calculated based on the standard apportionment method.

Kindly note that an Applicant seeking to use the SRP under the sectoral special method must provide a single recovery rate applicable to the entire Taxable Person, calculated based on the sectoral special method, in accordance with Article 55(16) of the Executive Regulation, which states that a Taxable Person may apply to use a SRP. Kindly refer to example in Appendix 1.

Validity period

An FTA decision approving the use of an SRP will be valid for four years and the Registrant will not be allowed to change the method for at least two years following the approval.

Applying for special apportionment method and/or SRP

Applications to use a special apportionment method and/or SRP have to be submitted via the Applicant's portal in EmaraTax.

Required information

The Applicant is required to provide the following information as part of the request:

A cover letter that includes the following:

A detailed description of the Business activities of the Applicant,

The special Input Tax apportionment method to be used, and

The reasons for applying for a special Input Tax apportionment method.

Historical calculations of Residual Input Tax apportionment in Excel format using the standard method of apportionment as provided in Article 55 of the Executive Regulation. The calculations should be for the period of 12 months preceding the application (as applicable). As an exception, if the Business has not conducted Business activities for at least 12 months, the calculations may be based on such shorter period.

Calculations of the Residual Input Tax apportionment in Excel format for the same period as above but using the special method for which the Applicant is applying, and an alternative method if applicable.

Where the application is made for a sectoral method, the Applicant must provide the special apportionment method calculations for each of the sectors for which the application is made as well as a description of each of the sectors.

The historical calculations of Residual Input Tax apportionment must be based on the actual figures of the Business for the relevant period of 12 months (where it is applicable). The values should agree to the amounts reflected in the Registrant's Tax Returns submitted during the Tax year. If there are any discrepancies, reasons for the variances have to be provided to the FTA.

As part of the calculations, the Applicant should provide information substantiating the figures which are used to perform apportionment calculations for both the standard method and the chosen special method(s). For example, if the calculation indicates that the Applicant made Exempt Supplies during the 12-month period, the Applicant should explain what type of Exempt Supplies it made and why the requested special apportionment method is considered to be the most appropriate method.

In the case of a request to use an SRP, the Applicant must also submit the annual adjustment calculations covering the preceding Tax year (i.e. annual washup calculation as well as the actual use adjustment calculation, if applicable), as well as the proposed SRP to be used for the subsequent Tax year.

Where a Registrant applies for approval to use an SRP in conjunction with a sectoral special Input Tax apportionment method, the following documents must be submitted together with the application:

The annual washup calculations for the preceding Tax year of application date, and

Such workings should include a breakdown of each sector' recovery rate and a single recovery rate (specifically for the applicable SRP rate) for the Registrant.

Please ensure that all the information provided in the calculations reconcile to the Tax Returns which have been submitted to the FTA for the relevant Tax Periods. Should there be any differences between the calculations and the Tax Returns, please provide detailed explanations for the reason and the nature of these differences.

Rejections, requests for further information and decisions

The FTA has the right to reject the application to use a special Input Tax apportionment method and/or the SRP or request further information if it is found that the application does not include all the relevant information or contains incorrect information.

Once the application is accepted, the FTA may require up to 40 Business Days from the date the application was received, to respond to the initial Input Tax apportionment application if a non-sectoral method is selected, and up to 60 Business Days if a sectoral method is selected.

If additional information is required in respect of the lodged application, the FTA will request the additional information. The Registrant must provide their response to the request of additional information within 40 Business Days, otherwise the request may be automatically closed in EmaraTax. It may take the FTA a further 40 or 60 Business Days (based on the method selected in the application) from the date all the requested information was received to respond to the updated request for a special Input Tax apportionment method and/or the SRP.

Furthermore, if the Registrant initiates the application to use a special Input Tax apportionment method and/or the SRP via the EmaraTax portal and the application is not completed and submitted to the FTA, the FTA will send an automated email to remind the Registrant to complete the draft application after 20 Business Days to finalise the application within 40 Business Days from the date of initiating the application. Note that the FTA may automatically close the request if it is not submitted within 40 Business Days from the date of initiating the application.[20]

If the issuance of the Input Tax apportionment decision is likely to take more than the period determined by the FTA, the FTA will inform the Applicant of the potential timeframe during which the Input Tax apportionment decision or the further information request decision shall be issued.

Kindly note that, in deciding whether to approve or reject the use of a special method and/or SRP, the FTA relies on the calculations submitted by the Applicant and does not review, nor verify, the numbers reported therein, nor the Tax treatments applied to transactions. The Applicant will have an obligation and is required to keep a record of the calculation in the event that the FTA undertakes an audit, in addition to reviewing relevant amendments to the applicable Tax legislation and guidance provided in respect of apportionment method. The Applicant will be notified of the FTA's decision via an email within 5 Business Days from the decision being made.

Validity period

Where the FTA has approved the use of a special Input Tax apportionment method and/or the SRP, the approved method and/or the SRP may be used from the first Tax Period following the date of approval, or any other date as decided by the FTA.

The approval to use a special Input Tax apportionment method will typically be granted for four years in the in the case of a non-sectoral method and for two years in the case of the sectoral method. Applicants cannot apply to change the approved method for at least two years following the approval, unless there is a significant change in the Business (see below).

An FTA decision approving the use of SRP will be valid for four years and the Registrant will not be allowed to change the apportionment method used to calculate the SRP for at least two years following the approval.

Note: The FTA may withdraw the approval to use a special Input Tax apportionment method and/or SRP at any time – for example, if it considers that the method does not provide an accurate result or where such withdrawal is necessary for the protection of public revenues. During the period of approval, the FTA may request from the Taxable Person such information as the FTA believes is necessary in order to make a decision regarding whether the ongoing use of the approved method is still appropriate or not.

Notifications relating to change in Business

A Registrant that receives approval to use a special apportionment method may not be required to perform an actual use calculation per Article 55(11) of the Executive Regulation for the duration of the validity period of the Decision issued by the FTA. However, Registrants are still required to ensure that the Input Tax recovered during each Tax year according to the annual washup aligns with the recovery rate submitted to the FTA at the time of applying for a special method.

Although a Registrant is generally not permitted to apply to change an approved special method for at least 2 years following receiving the approval from the FTA, it is required to notify the FTA where the recovery rate calculated during the full Tax year using the approved special method differs by more than 10% from the recovery rate provided to the FTA at the time of applying to use a special apportionment method. In such cases, the Registrant would be required to notify the FTA within 20 Business Days from the date on which such difference was identified. The Registrant's notification must include all of the following:

Confirmation of the variance and the date on which the Registrant identified the variance.

Reasons for the difference occurring.

Confirmation of any changes in the Business and operations of the Registrant.

The nature and details of these changes in the Registrant's Business and operations (if any).

Calculations for the full Tax year which have been used to identify the variance, including an annual washup calculation in Excel format.

Following the submission of the notification by the Registrant, the FTA will review the notification and supporting information and documents to consider whether the approved method is still suitable for the Registrant. Where the approved method is no longer considered suitable, the FTA may require the Registrant to submit a new Input Tax apportionment application.

The FTA may also request additional information relating to the notification and the Registrant will be required to provide a response within 40 Business Days.

Kindly note that if a Registrant fails to notify the FTA of a variance exceeding 10% within 20 Business Days or fails to provide a response to the FTA's request within 40 Business Days, the FTA may determine that the approved special method does not apply from the date on which a variance had been identified.

When to re-apply?

If the Registrant wants to continue using a special apportionment method and/or the SRP after the expiration of the previous decision, a new application must be submitted before the expiry of the most recent decision that approved the use of the special apportionment method and/or the SRP. Provided the Taxable Person submitted a request to continue using the previously approved special apportionment method before the decision's expiry date, the Registrant may continue using the previously approved method up to the end of the Tax Period during which a new decision on the request is issued by the FTA. However, should the Registrant fail to submit a renewal application before the expiry of the approved special apportionment method, the Applicant shall revert back to the standard inputs-based apportionment method from the day following the expiry thereof.

In case of any major change in the Business, the nature of the supplies and/or expense allocation principles, between the time of the original application data and the new application, such change should be highlighted to the FTA in the new application.

The new application shall include the same type of information and calculations as the original application, for a period of 12 months preceding the new application.

In the case of a request to use an SRP, the Applicant should submit the annual adjustment calculations for the preceding Tax year (i.e. annual washup calculation as well as the actual use adjustment calculation, if applicable), and the proposed SRP to be used for the subsequent Tax year.

In addition to the above, the new application shall contain a comparative overview of the recovery rates and sectors (where applicable) provided in the original application and in the new apportionment calculation requested, with an explanation of any major fluctuation in the recovery rates.

Updates and amendments

Date of amendment | Amendments made |

December 2019 | |

March 2023 |

|

June 2023 |

|

September 2025 |

|

Appendix 1: Input Tax apportionment examples

Please note that below are examples only and may not be suitable for, or may need to be adapted for specific cases.

Standard – inputs-based method

Standard (Inputs-based) method calculation | AED |

Total Input Tax (consolidated data for the whole Tax year) | XX |

Input Tax attributable to making Taxable Supplies (standard rated + zero-rated supplies) – Wholly Recoverable Input Tax | XX |

Input Tax attributable to making Exempt Supplies - non-recoverable | XX |

Input Tax blocked from recovery in line with the Article 53 of the Executive Regulation | XX |

Total Residual Input Tax - partially recoverable | XX |

Recovery percentage as per standard (inputs-based) method: | X% |

Recoverable Residual Input Tax | XX |

Non-recoverable Residual Input Tax: | XX |

Total Recoverable Input Tax for the period (Wholly Recoverable Input Tax + recoverable Residual Input Tax) | - |

Total recovered Input Tax as per the submitted Tax Returns | - |

Outputs-based method

Actual use calculation - Outputs-based method | AED |

Total Input Tax (consolidated data for the whole Tax year) | XX |

Wholly Recoverable Input Tax: | XX |

Non-recoverable Input Tax | XX |

Total Residual Input Tax | XX |

Special method: | |

Total Taxable Supplies | XX |

• Total standard-rated supplies | XX |

• Total zero-rated supplies | XX |

Total Exempt Supplies | XX |

Total non-business income | XX |

Recovery percentage as per outputs-based method: | X% |

Recoverable Residual Input Tax - outputs-based method: | XX |

Non-recoverable Residual Input Tax: | XX |

Total Recoverable Input Tax as per the actual use calculation (i.e. Wholly Recoverable Input Tax + recoverable Residual Input Tax): | - |

Transaction count method

Actual use calculation - Transaction count method | AED |

Total Input Tax (consolidated data for the whole Tax year) | XX |

Wholly Recoverable Input Tax: | XX |

Non-recoverable Input Tax | XX |

Total Residual Input Tax | XX |

Special method: | |

Number of taxable transactions | XX |

Total number of transactions | XX |

Recovery percentage as per transaction count method: | X% |

Recoverable Residual Input Tax - transaction count method: | XX |

Non-recoverable Residual Input Tax: | XX |

Total Recoverable Input Tax as per the actual use calculation (i.e. Wholly Recoverable Input Tax + recoverable Residual Input Tax): | - |

Floorspace method

Actual use calculation - Floorspace method | AED |

Total Input Tax (consolidated data for the whole Tax year) | XX |

Wholly Recoverable Input Tax: | XX |

Non-recoverable Input Tax | XX |

Total Residual Input Tax | XX |

Special method: | |

Total amount of floorspace (m2) used by Taxpayer | XX |

Floorspace (m2) used for making Taxable Supplies | XX |

Floorspace (m2) used for making Exempt Supplies | XX |

Communal areas (m2) | XX |

Floorspace (m2) used for making both Taxable Supplies and Exempt Supplies | XX |

Recovery percentage as per floorspace method: | X% |

Recoverable Residual Input Tax - floorspace method: | XX |

Non-recoverable Residual Input Tax: | XX |

Total Recoverable Input Tax as per the actual use calculation (i.e. Wholly Recoverable Input Tax + recoverable Residual Input Tax): | - |

Sectoral method

Original - Special method application | New application - Special method application | ||||

Tax period covered: | 1 July 2019 - 30 June 2020 | Tax period covered: | 1 July 2021 - 30 June 2022 | ||

Method selected: | Sectoral | Method selected: | Sectoral | ||

Description: | Amount (AED) | VAT (AED) | Description: | Amount (AED) | VAT (AED) |

Total value of the Input VAT for the period: | Total value of the Input VAT for the period: | ||||

a. Input tax wholly attributable to making standard rated supplies: | a. Input tax wholly attributable to making standard rated supplies: | ||||

b. Input tax wholly attributable to making zero rated supplies: | b. Input tax wholly attributable to making zero rated supplies: | ||||

Input tax wholly attributable to making taxable supplies (a. + b.): | Input tax wholly attributable to making taxable supplies (a. + b.): | ||||

Input tax wholly attributable to making exempt supplies: | Input tax wholly attributable to making exempt supplies: | ||||

Total value of the overheads / residual Input tax: | Total value of the overheads / residual Input tax: | ||||

Sector allocation – directly attributable overheads / residual Input tax: | Amount (AED) | VAT (AED) | Sector allocation – directly attributable overheads / residual Input tax: | Amount (AED) | VAT (AED) |

Sector I: | Sector I: | ||||

Sector II: | Sector II: | ||||

Sector III: | Sector III: | ||||

Sector IV: | Sector IV: | ||||

Sector V: | Sector V: | ||||

Remaining unallocated Input tax overheads / residual Input tax: | Remaining unallocated Input tax overheads / residual Input tax: | ||||

Overheads / residual input tax allocation method: | Headcount or Outputs method | Overheads / residual input tax allocation method: | Headcount or Outputs method | ||

Explanation on why certain allocation method has been selected (e.g. make sure to provide headcount overview): | Explanation on why certain allocation method has been selected (e.g. make sure to provide headcount overview): | ||||

Application of the sector allocation methodology on the overheads / residual input tax allocation to sectors: | Amount (AED) | VAT (AED) | Application of the sector allocation methodology on the overheads / residual input tax allocation to sectors: | Amount (AED) | VAT (AED) |

Sector I: | Sector I: | ||||

Sector II: | Sector II: | ||||

Sector III: | Sector III: | ||||

Sector IV: | Sector IV: | ||||

Sector V: | Sector V: | ||||

Consolidated - Sector allocation on the overheads / residual input tax: | Consolidated - Sector allocation on the overheads / residual input tax: | ||||

Sector I: | Sector I: | ||||

Sector II: | Sector II: | ||||

Sector III: | Sector III: | ||||

Sector IV: | Sector IV: | ||||

Sector V: | Sector V: | ||||

Consolidated - Sector Input tax recovery | Consolidated - Sector Input tax recovery | ||||

Sector | Input tax - recovery percentage | Recoverable Input tax for the period | Sector | Input tax - recovery percentage | Recoverable Input tax for the period |

Sector I: | Sector I: | ||||

Sector II: | Sector II: | ||||

Sector III: | Sector III: | ||||

Sector IV: | Sector IV: | ||||

Sector V: | Sector V: | ||||

Comparative overview of the special method application

| Sectors: | Recovery rate as per the previously approved special method | Recovery rate as per the new special method application | Comments on the major differences between the recovery rates |

|---|---|---|---|

| Sector I: | |||

| Sector II: | |||

| Sector III: | |||

| Sector IV: | |||

| Sector V: |

SRP based on a sectoral special apportionment method - Example

An Applicant operates across 4 different sectors, and has a Tax year that ends on 31 December and applied to use the SRP. The Applicant incurred Residual Input Tax of AED 1,200,000 during the 2024 Tax year. After completing the calculations for its year-end adjustments for the 2024 Tax year using the sectoral method, the recovery rate for the full year was 67%, calculated as follows:

Sector | Method | Residual Input Tax allocated | Residual Input Tax recovered per sector using the special method |

Sector 1 | Based on transaction count | 228,000 | 38,760 (17%) |

Sector 2 | Based on outputs | 144,000 | 21,600 (15%) |

Sector 3 | Based on outputs | 480,000 | 480,000 (100%) |

Sector 4 | Based on floorspace | 348,000 | 261,000 (75%) |

Total | 1,200,000 (A) | 801,360 (B) |

Based on the above, as part of the annual washup calculation, the recovery rate for Residual Input Tax is calculated as 801,360/1,200,000, i.e. 67%.

If the FTA approved the use of SRP based on the sectoral special apportionment method, the Applicant will recover 67% of the Residual Input Tax during each of the Tax Periods during the 2025 Tax year. At the end of the 2025 Tax year, the Applicant would be required to perform an annual washup calculation based on sectoral special apportionment method. The recovery rate determined as a result of this annual washup will constitute the SRP for the 2026 Tax year.

Appendix 2: Common errors/checklist

Based on the Input Tax apportionment special method requests received, the FTA has identified errors that are common across applications. The checklist below can be used to assist Applicants with submitting a complete application, and avoid submitting incomplete or incorrect applications and/or supporting documents:

General checks that apply to Applicants for all methods:

Provide a signed letter by the authorised signatory confirming the request to apply for the special method.

Submit the standard method and the proposed method calculations in Excel format for a period of 12 months preceding the application (where it is applicable). The calculations should be done for each Tax Period separately and also consolidated for the entire 12-month period (where it is applicable). Furthermore, please use Excel formulae for the calculations.

Ensure that the recovery rate percentages are rounded to the nearest whole number in accordance with Article 55(7)(b) of the Executive Regulation.

Clearly identify in the calculations the expenses that are wholly attributable to either Exempt Supplies or Taxable Supplies or residual. This also applies to expenses which are subject to the reverse charge mechanism.

Make sure that there are no deviations between the calculations provided and the submitted Tax Returns. If there are any deviations, they should be clearly explained.

Standard method

Exclude Input Tax that is non-recoverable under Article 53 of the Executive Regulation from the standard method calculations.

Outputs-based method

Exclude transactions which are subject to the reverse charge mechanism that would be reported under Boxes 3, 6 and 7 of the Tax Return from the outputs-based method calculations. Reverse charge mechanism, generally, relates to the payment of VAT upon the importation of Goods and Services into the UAE. Although the payment of VAT under the reverse charge mechanism is disclosed under the Output Tax section of the Tax Return, these are considered as expenses for the purposes of apportionment calculation.

Transaction count method

Exclude expense transactions when performing the transaction count method calculations.

Exclude transactions which are subject to the reverse charge mechanism that would be reported under Boxes 3, 6 and 7 of the Tax Return. Reverse charge mechanism, generally ,relates to the payment of VAT upon the importation of Goods and Services into the UAE. Although the payment of VAT under the reverse charge mechanism is disclosed under the Output Tax section of the Tax Return, these are considered as expenses for the purposes of apportionment calculation.

Floorspace method

Exclude communal areas such as lobbies and lifts when calculating the floorspace available for commercial or residential use.

Sectoral method

Allocations:

State the methodology used to allocate Residual Input Tax across different sectors.

If the headcount method is the chosen allocation method, provide a breakdown of the total headcount. This should reflect the total front and back-office staff as well as any contracted personnel, even if not all of these staff are used in the headcount allocation calculations.

Sectors:

Provide detailed information on the activities performed by each sector.

Attach the calculations showing how the recoverability percentage for each sector has been derived.

Include the apportionment methods used for each sector along with the rationale for using each method.

GTL Notes

[G1]We believe that this is an incorrect reference and the correct reference is Appendix 1

[G2]We believe that this is an incorrect reference and the correct reference is Appendix 2