Issue

Corporate Tax in the UAE is regulated by Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses, and its amendments ("Corporate Tax Law").

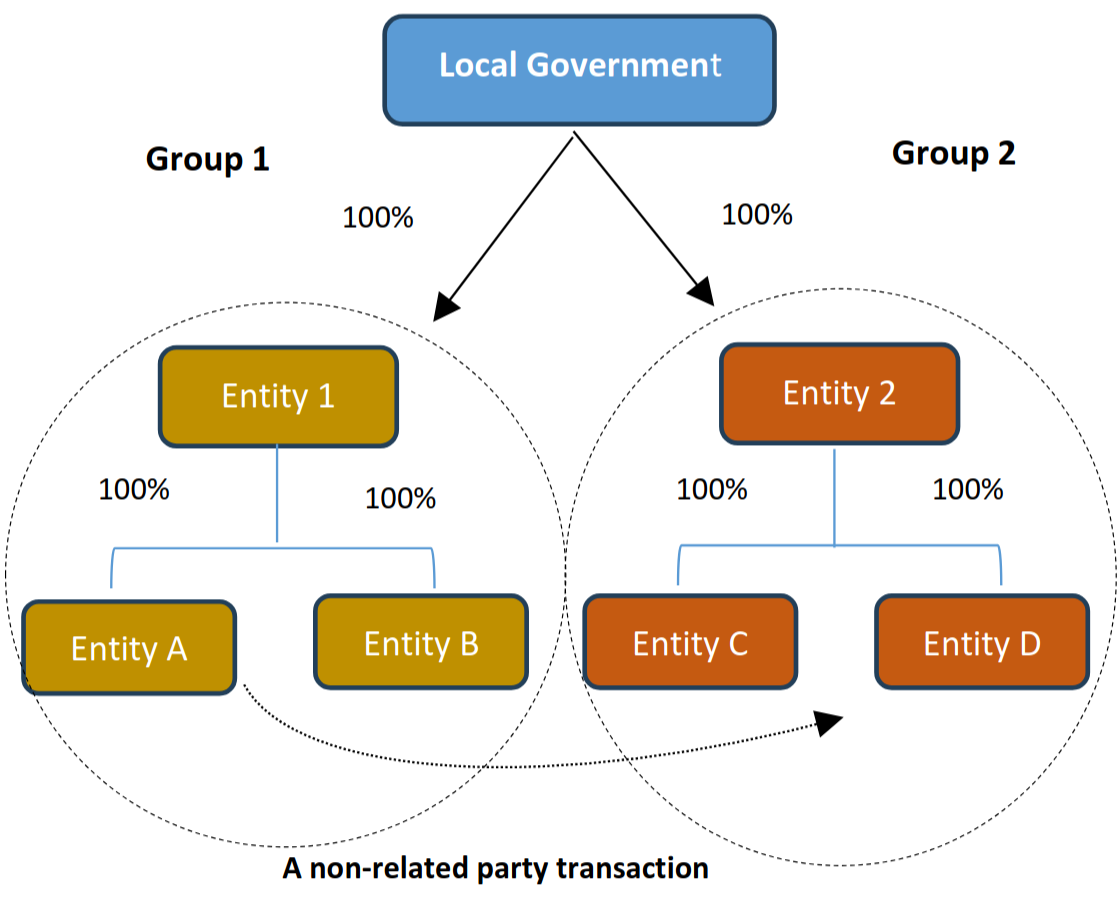

As per Article 34 of the Corporate Tax Law, in determining Taxable Income, transactions and arrangements between Related Parties must meet the arm's length standard.

Article 35 of the Corporate Tax Law provides the definition of "Related Parties". Based on this definition, two or more juridical persons can be Related Parties as a result of common ownership and/or Control, whether direct or indirect.

This Public clarification explains the application of the Related Parties definition as per Article 35 of the Corporate Tax Law to structures where common ownership and/or Control is by virtue of the UAE Federal Government or a Local Government (i.e. Emirate-level government).