Contents

1. What is a VAT return?

2. Who files VAT returns and when?

3. How do Taxpayers complete VAT return forms?

4. Where can Taxpayers refer to further information on VAT return filing?

Appendix - Simplified VAT Filing Scenarios

Simplified filing Scenarios

KSA Shop (1/4)

KSA Shop (2/4)

KSA Shop (3/4)

KSA Shop (4/4)

KSA Chemicals Manufacturer (1/2)

KSA Chemicals Manufacturer (2/2)

KSA Car Manufacturer and Finance Provider (1/2)

KSA Car Manufacturer and Finance Provider (2/2)

Change of VAT rate to 15% as of July 1, 2020

Upon the introduction of VAT in January 2018, the KSA applied a basic VAT rate of 5% to Taxable Supplies and Imports made in the Kingdom. The basic VAT rate was revised to 15% with effect from 1 July 2020 (the “Revised VAT Rate”).

Transitional rules have been introduced to clarify the VAT rate to be applied to long-term contracts for continuous supplies which span 1 July 2020, and for certain supplies where invoices are issued or contracts are concluded prior to 11 May 2020. These rules, and further detail surrounding the change to the VAT rate -including guidance in respect of specific types of supply- are detailed in a separate guideline on the Revised VAT Rate.

This Guideline was originally issued before the VAT rate was revised to 15%, and its content is based on the 5% rate in force at the time of its issue. Any references to the 5% VAT rate in this Guideline should be interpreted as 15% where applied to any Supplies or Imports made on or after 1 July 2020 and in accordance with the transitional rules. Monetary examples or calculations in this Guideline which include a 5% VAT rate should also be interpreted as if the 15% rate applied for all Supplies or Imports made on or after 1 July 2020 and in accordance with the transitional rules.

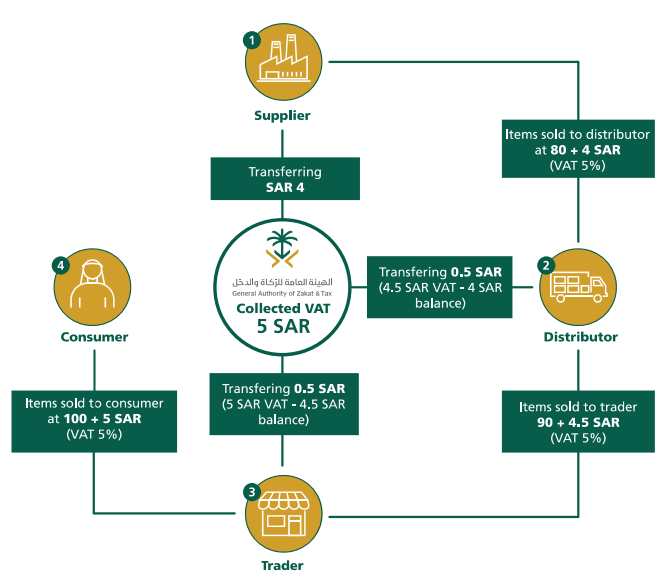

What is a VAT return?

VAT is collected throughout the value chain, where companies record the VAT revenue they collect via a VAT return form submitted to GAZT.

VAT Collection across the Supply Chain

Completed VAT Return Forms

* For illustrative purposes only

Who files VAT returns and when?

A business' volume of annual taxable supplies determines when it needs to start filing, as well as the frequency of its filing obligations.

Annual Taxable Supplies of VAT-Registered Businesses