Beta Version

Website Last updated:

July 10, 2026

Simplified Guide

The Decision to Reclassify the Value-Added Tax Field Violations

Zakat, Tax and Customs Authority

January 30, 2022

Contents

1. Highlights of the Decision

2. What Is Not Covered by the Decision?

3. Classification of Violations According to the New Decision

4. Illustrative Examples of the Decision to Reclassify VAT Violations

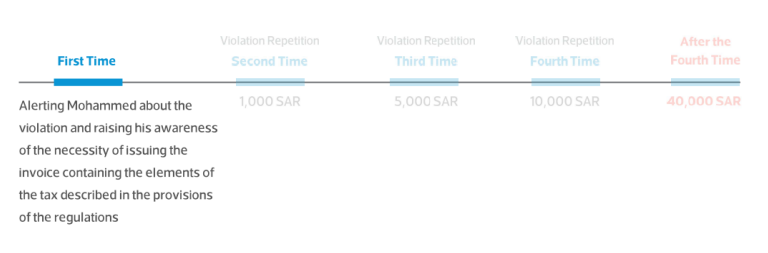

First: Violation of non-compliance to issue a tax invoice

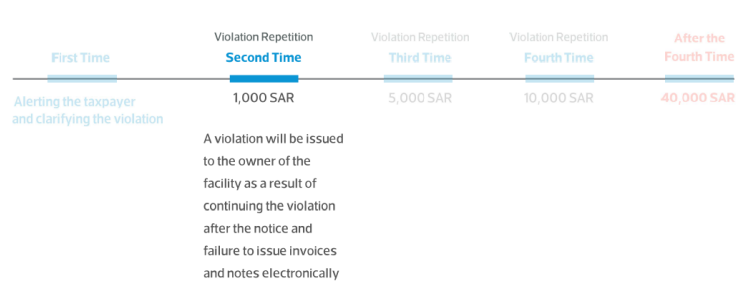

Second: Violation of not issuing and keeping invoices and notes electronically

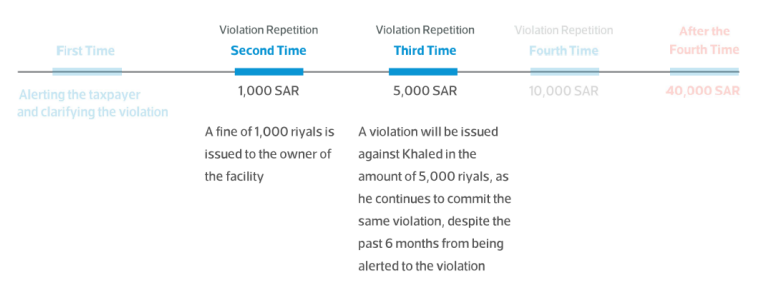

Third: Violation of not keeping invoices, records and accounting documents

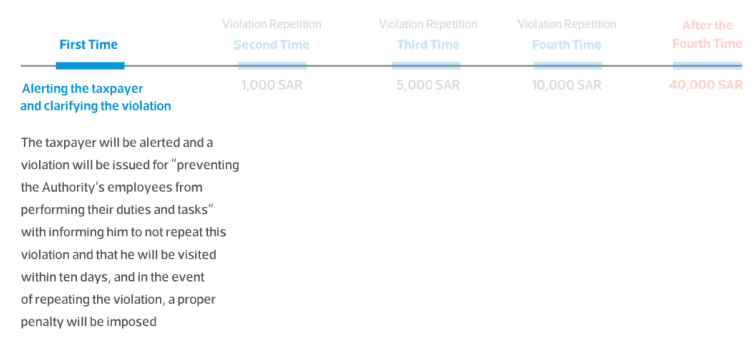

Fourth: Violation of Preventing or hindering the Authority's employees from performing their job duties and tasks

Fifth: Violation of incorrectly calculating the due tax

Sixth: Violation of not notifying the Authority of any malfunctions that hinder the process of issuing invoices and electronic notes

Seventh: Violation of deleting invoices or electronic notes

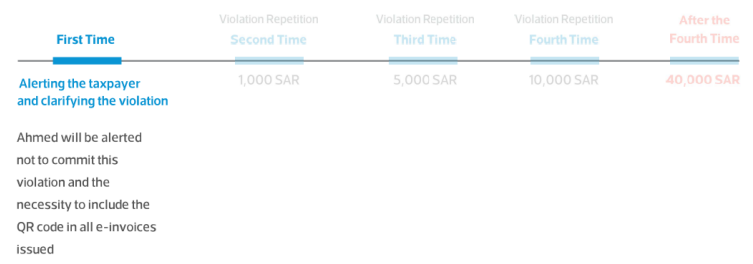

Eighth: Violation of not including the QR code in the e-invoice

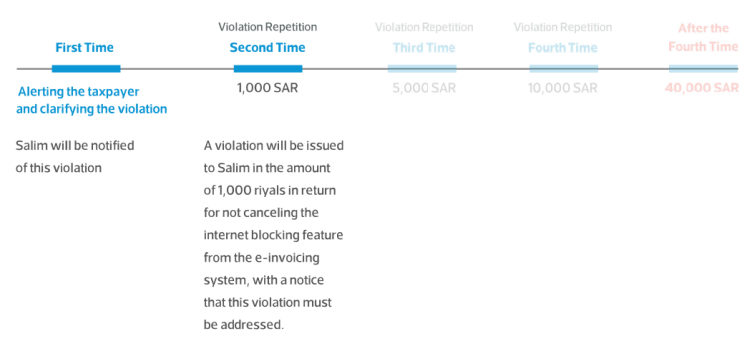

Ninth: Violation of including any of the prohibited functions in the e-invoicing system used to issue and save invoices electronically

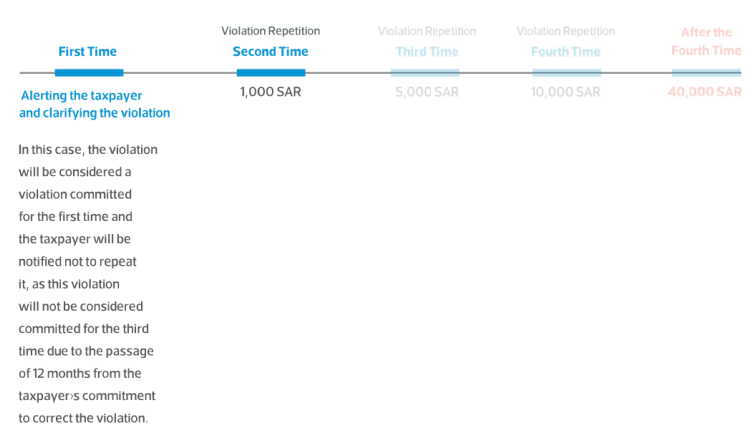

Tenth: An illustrative example of what was stated in the decision regarding calculating fines for violations that have been repeated 12 months after the taxpayer committed it

The Zakat, Tax and Customs Authority ("ZATCA", "Authority“) has issued this Guide for the purpose of clarifying certain tax treatments concerning the implementation of the statutory provisions in force as of the Guide's issue date. The content of this Guide shall not be considered as an amendment to any of the provisions of the Laws and Regulations applicable in the Kingdom.

Furthermore, the Authority would like to highlight that the clarifications and indicative tax treatments prescribed in this Guide, where applicable, shall be implemented by the Authority in light of the relevant statutory texts. Where any clarification, interpretation or content provided in this Guide is modified - in relation to unchanged statutory text - the updated indicative tax treatment shall then be applicable prospectively, in respect of transactions made after the publication date of the updated version of the Guide on the Authority's website.