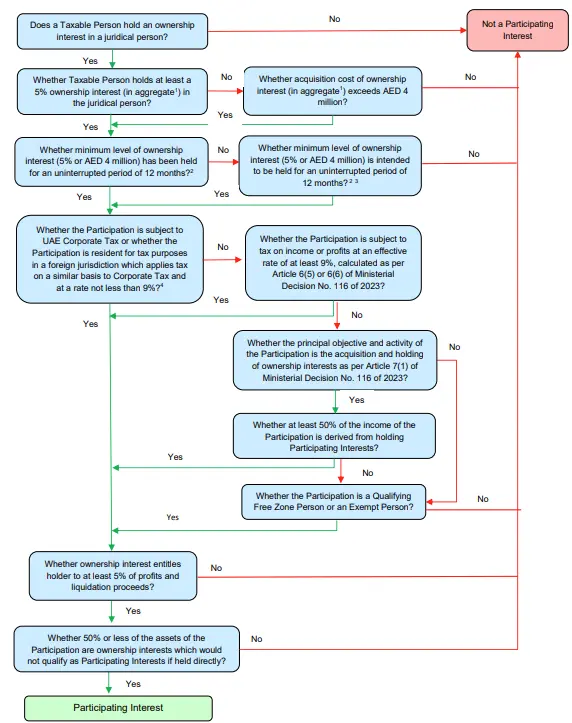

Figure 2: Overview of conditions to qualify as a Participating Interest

Website Last updated:

July 3, 2026

1. Glossary

2. Introduction

2.1. Overview

2.2. Purpose of this guide

2.3. Who should read this guide?

2.4. How to use this guide

2.5. Legislative references

2.6. Status of this guide

3. Dividends and other profit distributions

3.1. What is a Dividend?

3.1.1. Overview

3.1.2. Ordinary Dividend

3.1.3. Payments that do not qualify as a Dividend

3.1.4. Dividend in kind

3.1.5. Other distributions

3.1.6. Non-arm’s length: constructive Dividend

3.2. Taxation of Dividends and other profit distributions

3.2.1. Personal Investment income (natural person only)

3.2.2. Dividend from a Resident Person

3.2.3. Foreign Dividends

4. Participation Exemption: overview

4.1. Introduction

4.2. Definition of Participating Interest

4.3. Exempt Income and losses

4.4. Automatic exemption: no election required

4.5. Availability of exemption to both Resident Person and Non-Resident Person

5. Participation Exemption: definition of Participating Interest

5.1. Ownership interest test

5.1.1. What is an ownership interest?

5.1.2. Debt instruments issued by the Participation

5.1.3. Options

5.1.4. Owner of ownership interests

5.2. Minimum ownership test

5.2.1. Computation of percentage ownership

5.2.2. Aggregation of Qualifying Group holdings

5.2.3. Falling below the 5% ownership threshold

5.3. Holding period test

5.3.1. Intention to hold Participating Interest for at least 12 months

5.3.2. Different ownerships interests in a juridical person held for different periods

5.3.3. Transfer of ownership interest in case of business restructuring

5.3.4. Required holding period exceptions

5.4. Minimum acquisition cost test

5.4.1. Aggregation of acquisition costs

5.4.2. Computation of acquisition cost

5.5. Subject to tax test

5.5.1. Subject to Corporate Tax or similar

5.5.2. Foreign tax rate of at least 9%

5.6. Exceptions to the subject to tax test

5.6.1. Qualifying Free Zone Persons and Exempt Persons

5.6.2. Holding companies

5.6.3. Small Business Relief

5.7. Entitlement to profits and liquidation proceeds test

5.8. Asset test

6. Participation Exemption: Exempt Income and loss